HSA Tax Benefits Triple Advantage: The Best-Kept Secret in Personal Finance

Advertisements

Here’s a stat that honestly blew my mind when I first stumbled across it — less than 10% of HSA holders actually invest their funds for long-term growth. That means the vast majority of people are sitting on what’s arguably the most powerful tax-advantaged account in the entire U.S. tax code and barely scratching the surface. I’ll be real with you, I was one of those people for years!

The HSA tax benefits triple advantage is something I wish someone had explained to me back when I first enrolled in a high-deductible health plan. I literally used my Health Savings Account like a glorified checking account for copays. So let me break down what I’ve learned — the hard way — and why this triple tax benefit deserves way more attention than it gets.

What Exactly Is the HSA Triple Tax Advantage?

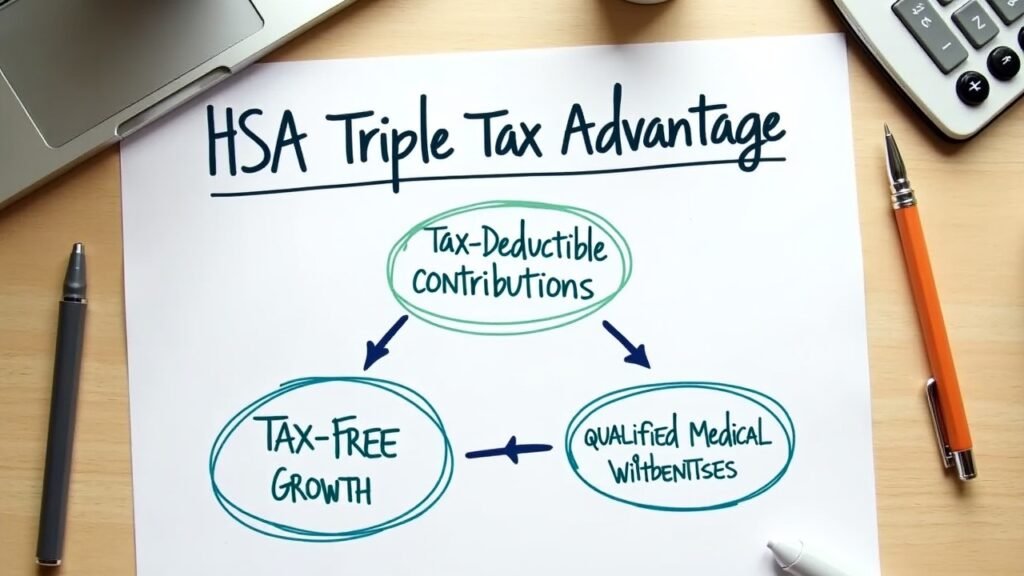

Okay, so the “triple advantage” isn’t some marketing gimmick. It’s genuinely three separate tax benefits stacked on top of each other, and no other account in the country offers all three simultaneously. Not your 401(k), not your Roth IRA — nothing.

Here’s how it breaks down:

- Tax-deductible contributions: The money you put into your HSA reduces your taxable income for the year. If you contribute through payroll deductions, you also skip FICA taxes, which is something even a traditional IRA can’t do.

- Tax-free growth: Any interest, dividends, or investment gains inside your HSA grow completely tax-free. No capital gains taxes. Nothing.

- Tax-free withdrawals: When you pull money out for qualified medical expenses, you pay zero taxes on it. Zero!

The IRS outlines the full rules for HSAs in Publication 969, and honestly it’s worth a skim even though it’s a little dry. Understanding the contribution limits and eligibility requirements saved me from a costly mistake once.

My Biggest HSA Mistake (Don’t Repeat It)

So back in 2019, I had about $4,200 sitting in my HSA. Every time I had a doctor visit or picked up a prescription, I’d swipe that HSA debit card immediately. Felt smart at the time — free money for healthcare, right?

Wrong. Well, not wrong exactly, but I was leaving so much on the table. A coworker mentioned she was investing her HSA funds in index funds and paying for medical expenses out of pocket instead. My first reaction was honestly confusion. Why would you NOT use the account that’s literally designed for medical bills?

Then she explained the long game. By letting those invested funds grow tax-free for decades, she was essentially building a medical retirement fund. The Fidelity Retiree Health Care Cost Estimate suggests a 65-year-old couple will need roughly $315,000 for healthcare in retirement. That number is terrifying, but it’s also exactly why the HSA triple tax advantage matters so much.

How to Actually Maximize the Triple Tax Benefit

After that wake-up call, I completely changed my approach. Here’s what’s been working for me and what I’d recommend to anyone who’s eligible:

Advertisements

- Max out your contributions every year. For 2025, the limits are $4,300 for individual coverage and $8,550 for family coverage. If you’re 55 or older, you get an extra $1,000 catch-up contribution.

- Invest the balance. Most HSA providers offer investment options once you hit a certain threshold. I keep about $1,000 in cash for near-term expenses and invest everything else in a low-cost total market index fund.

- Pay medical expenses out of pocket when possible. Save your receipts. There’s no time limit on reimbursing yourself from your HSA, so you could technically reimburse yourself years later while those funds have been compounding tax-free.

- Keep every single receipt. I use a simple folder in Google Drive. It’s not glamorous, but if the IRS ever comes knocking, you’ll be glad you did.

One thing that tripped me up — you MUST be enrolled in a qualifying high-deductible health plan (HDHP) to contribute to an HSA. No HDHP, no contributions. That’s non-negotiable.

Why This Matters More Than You Think

Look, I’m not a financial advisor and everyone’s situation is different. But the HSA triple tax advantage is one of those rare tools that benefits you at every single stage — when money goes in, while it grows, and when it comes out. That’s powerful stuff.

My only regret is not taking it seriously sooner. Whether you’re 25 or 55, it’s worth looking into how an HSA fits your overall tax strategy and retirement planning. Do your own research, talk to a tax professional, and make sure the numbers work for your specific circumstances.

If you found this helpful and want to dig deeper into tax strategies that can actually save you real money, check out more posts on Deduction Desk. We’re always breaking down this stuff in plain English — because nobody should need an accounting degree just to keep more of their own money.